All Categories

Featured

Table of Contents

Of training course, there are other advantages to any type of entire life insurance coverage plan. While you are trying to decrease the proportion of premium to death benefit, you can not have a policy with no death advantage.

Some individuals marketing these plans suggest that you are not disrupting compound interest if you obtain from your plan instead of take out from your savings account. That is not the instance. It interrupts it in exactly the exact same means. The cash you obtain out earns nothing (at bestif you do not have a laundry car loan, it might also be costing you).

A lot of the people that buy right into this idea also acquire right into conspiracy theories concerning the globe, its governments, and its banking system. IB/BOY/LEAP is placed as a means to in some way avoid the globe's economic system as if the world's biggest insurance policy firms were not component of its economic system.

It is spent in the general fund of the insurance policy firm, which mostly invests in bonds such as US treasury bonds. You get a bit higher rate of interest price on your cash money (after the very first couple of years) and maybe some asset defense. Like your financial investments, your life insurance policy should be uninteresting.

Royal Bank Infinite Avion Points

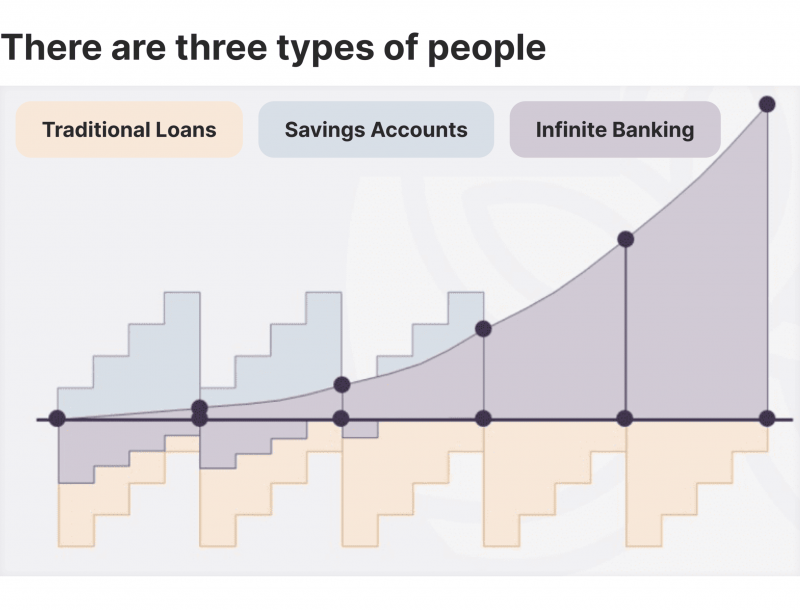

It appears like the name of this concept modifications when a month. You may have heard it referred to as a perpetual wide range approach, household financial, or circle of wealth. No matter what name it's called, unlimited financial is pitched as a secret method to construct wealth that just abundant individuals find out about.

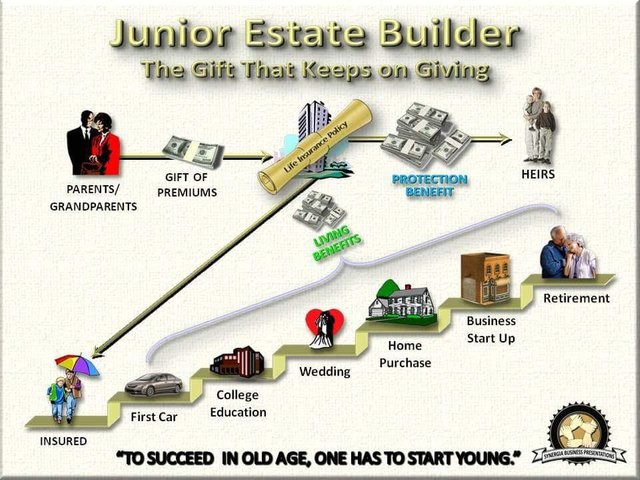

You, the insurance policy holder, put money into a whole life insurance plan with paying costs and purchasing paid-up additions. This increases the cash value of the policy, which implies there is more cash for the reward rate to be related to, which normally suggests a higher price of return on the whole. Returns prices at significant service providers are currently around 5% to 6%.

Infinite Banking Videos

The whole concept of "financial on yourself" only functions since you can "bank" on yourself by taking lendings from the policy (the arrow in the graph over going from entire life insurance policy back to the policyholder). There are two various kinds of financings the insurer might use, either direct recognition or non-direct recognition.

One attribute called "wash finances" establishes the rate of interest on loans to the exact same rate as the dividend rate. This indicates you can obtain from the plan without paying passion or receiving passion on the quantity you borrow. The draw of boundless financial is a dividend rates of interest and guaranteed minimum rate of return.

The disadvantages of boundless financial are typically neglected or not pointed out at all (much of the info offered regarding this idea is from insurance representatives, which might be a little prejudiced). Just the money value is growing at the dividend rate. You likewise have to pay for the price of insurance policy, costs, and costs.

Companies that supply non-direct recognition loans may have a reduced returns rate. Your money is locked into a complicated insurance item, and abandonment charges typically do not vanish up until you have actually had the policy for 10 to 15 years. Every long-term life insurance policy plan is various, however it's clear somebody's total return on every buck invested in an insurance policy product could not be anywhere near the dividend rate for the policy.

Infinite Banking Concept Book

To give an extremely fundamental and theoretical example, let's presume somebody is able to make 3%, on standard, for every buck they spend on an "unlimited banking" insurance coverage item (after all expenditures and charges). If we assume those bucks would certainly be subject to 50% in tax obligations amount to if not in the insurance item, the tax-adjusted rate of return can be 4.5%.

We presume greater than average returns on the whole life product and a very high tax price on bucks not place right into the policy (which makes the insurance item look far better). The reality for numerous folks might be even worse. This pales in contrast to the long-term return of the S&P 500 of over 10%.

Royal Bank Visa Infinite Avion Travel Rewards

At the end of the day you are buying an insurance item. We like the protection that insurance coverage supplies, which can be acquired a lot less expensively from a low-cost term life insurance plan. Unpaid finances from the plan might additionally lower your survivor benefit, lessening another degree of protection in the plan.

The concept just works when you not just pay the significant costs, yet make use of extra cash money to buy paid-up enhancements. The opportunity expense of all of those dollars is significant incredibly so when you could rather be spending in a Roth Individual Retirement Account, HSA, or 401(k). Even when compared to a taxed investment account or even an interest-bearing account, unlimited banking may not supply similar returns (contrasted to spending) and equivalent liquidity, access, and low/no fee framework (compared to a high-yield cost savings account).

When it involves monetary preparation, whole life insurance policy typically attracts attention as a popular choice. However, there's been a growing pattern of advertising it as a device for "unlimited banking." If you've been discovering entire life insurance coverage or have actually found this concept, you could have been informed that it can be a method to "become your own bank." While the concept could seem attractive, it's essential to dig deeper to understand what this truly implies and why viewing whole life insurance policy in this means can be deceptive.

The concept of "being your very own bank" is appealing since it suggests a high level of control over your financial resources. This control can be illusory. Insurance coverage companies have the supreme say in exactly how your plan is taken care of, including the regards to the financings and the prices of return on your cash money worth.

If you're thinking about whole life insurance policy, it's vital to view it in a wider context. Entire life insurance policy can be a useful tool for estate planning, giving a guaranteed survivor benefit to your recipients and potentially providing tax benefits. It can likewise be a forced savings lorry for those who have a hard time to save money regularly.

Royal Bank Infinite Avion Travel Rewards

It's a form of insurance with a financial savings element. While it can provide constant, low-risk development of money value, the returns are usually lower than what you could achieve with other financial investment cars. Before delving into entire life insurance policy with the idea of infinite banking in mind, make the effort to consider your economic objectives, danger resistance, and the full array of financial items offered to you.

Limitless banking is not an economic cure all. While it can operate in specific circumstances, it's not without dangers, and it requires a considerable dedication and comprehending to manage successfully. By recognizing the prospective risks and recognizing the true nature of whole life insurance policy, you'll be better furnished to make an enlightened decision that sustains your economic health.

This book will certainly show you just how to establish up a financial plan and just how to utilize the banking plan to spend in actual estate.

Infinite financial is not a services or product used by a details organization. Boundless banking is a method in which you buy a life insurance coverage policy that gathers interest-earning money value and obtain car loans against it, "borrowing from yourself" as a source of funding. After that at some point pay back the finance and begin the cycle throughout once again.

Pay policy costs, a part of which develops cash money worth. Take a car loan out versus the plan's money worth, tax-free. If you use this idea as meant, you're taking cash out of your life insurance policy to purchase whatever you 'd require for the remainder of your life.

{kind=link}

Latest Posts

Infinite Banking Spreadsheet

How To Start Your Own Personal Bank

Whole Life Concept Model